Content

61

Bluesky

05/13

Un simple "allo" oui, mais il faut étonnamment peu d'échantillons vocaux pour réussir une usurpation suffisamment convaincante que pour passer sur une ligne téléphonique où la basse qualité de la communication masque les défauts de la copie.

Un simple "allo" oui, mais il faut étonnamment peu d'échantillons vocaux pour réussir une usurpation suffisamment convaincante que pour passer sur une ligne téléphonique où la basse qualité de la comm...

Votes:

1

0

57

Yahoo Finance

05/13

(Community Post)

ALLO was mentioned in a positive light in MaxCyte's very upbeat CC yesterday. They work with Allogene supplying electroporation devices for them so they get their info through business orders, not message boards. I tried to post this earlier but it disappeared. Weird. Not financial advice, it just sounded good to me....

Votes:

2

0

57

Yahoo Finance

05/13

(Community Post)

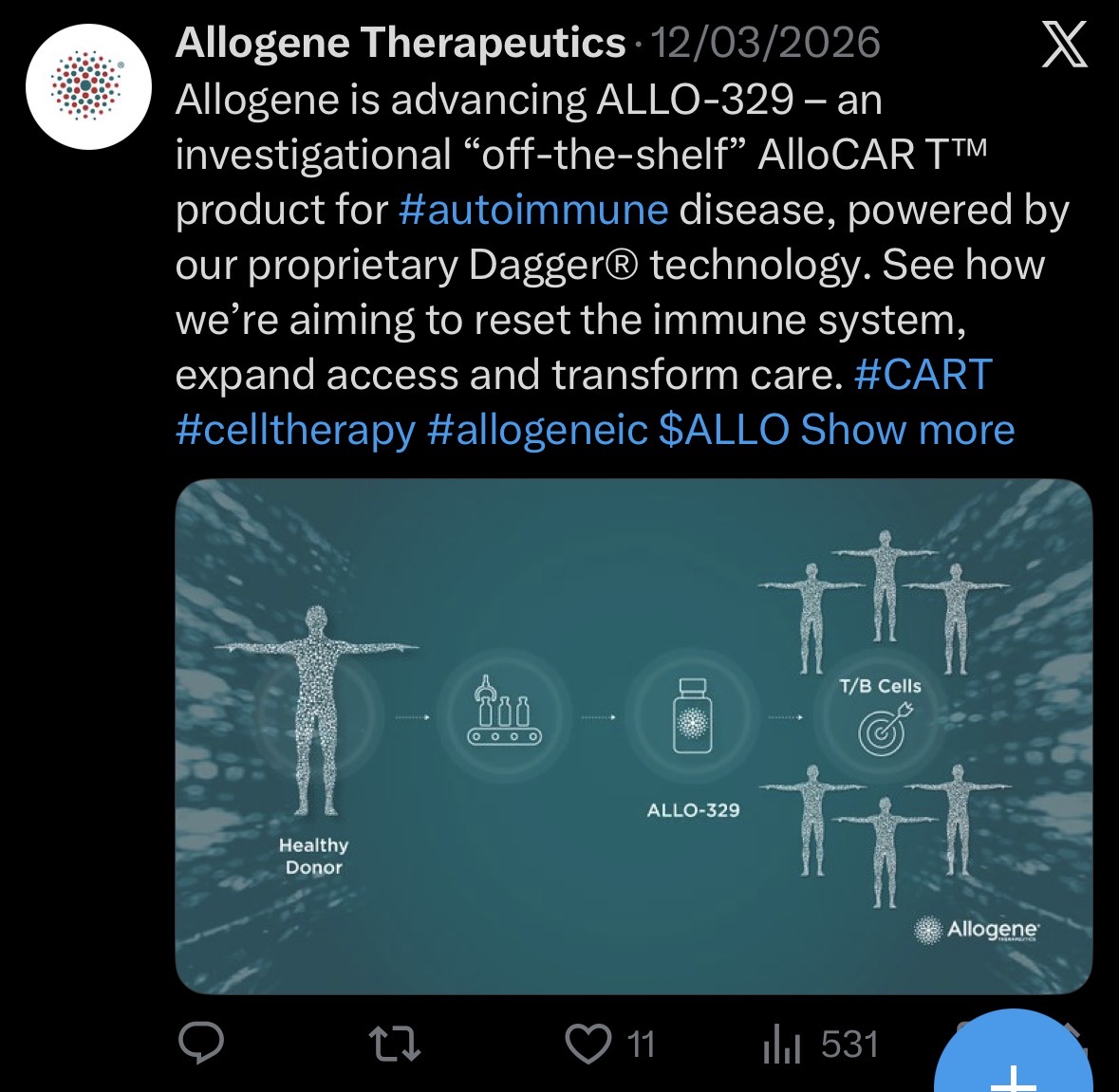

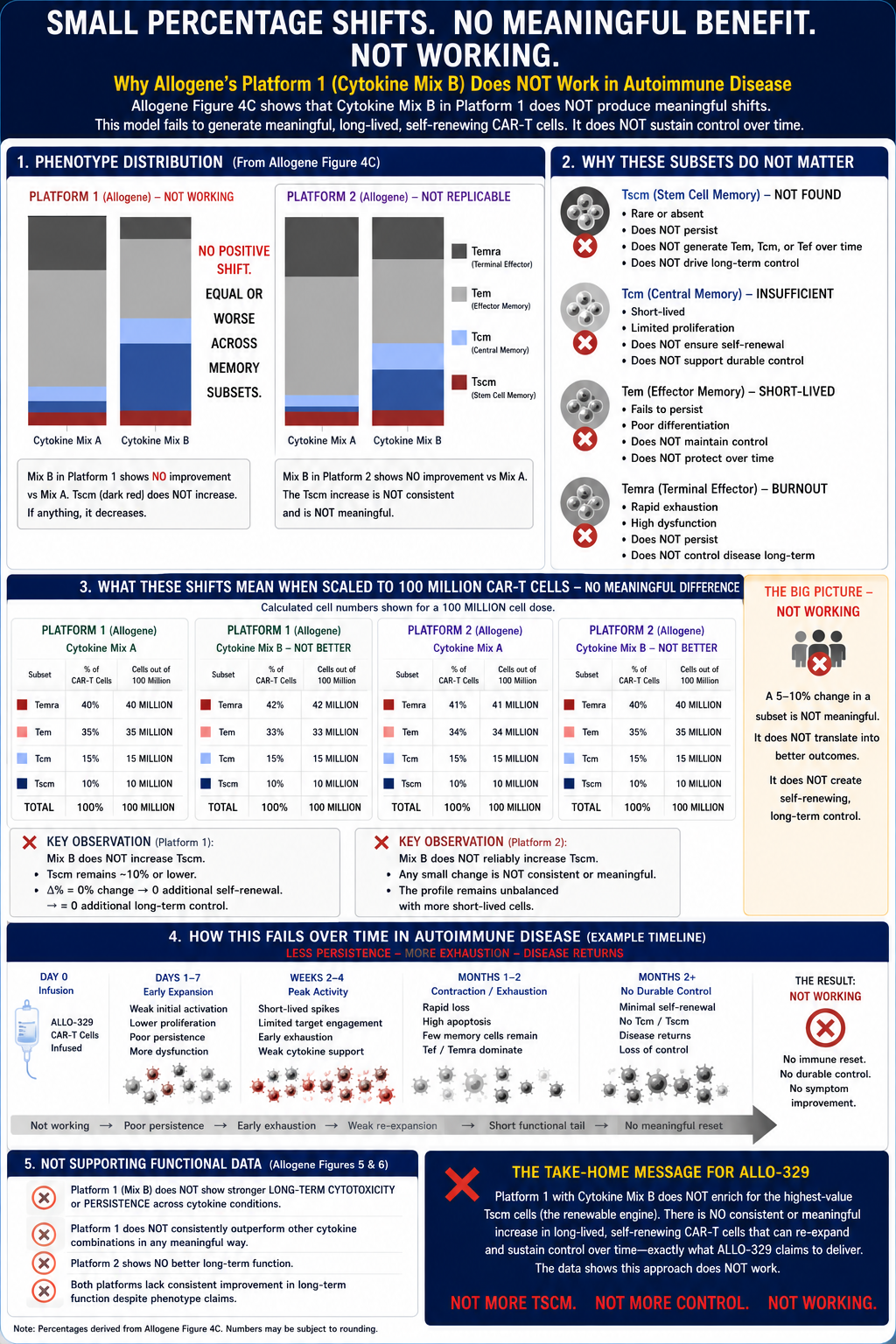

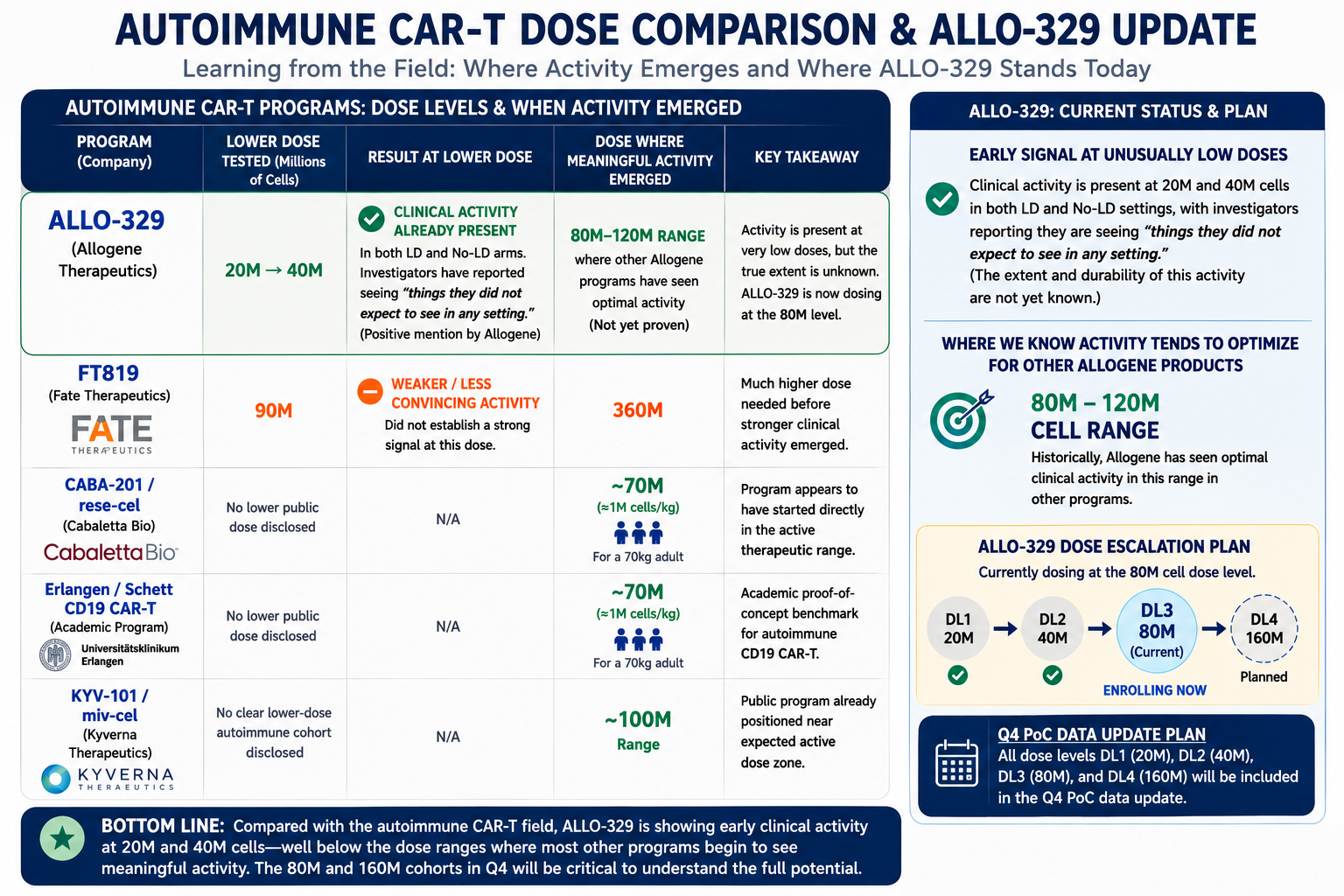

What this infographic below is really showing is that small differences in CAR-T cell quality can become very important when scaled across millions of cells inside a patient. This is what Allogene is presenting tonight in Boston at ASGCT 2026. Allogene’s data suggest their Platform 1 manufacturing approach creates more of the high value “younger” memory CAR-T cells (especially Tscm cells) that are associated with longer persistence, self-renewal, and repeated re-expansion over time. In autoimmune disease, that may matter more than having the biggest early expansion spike because the goal is not just rapid killing on Day 1 - it is maintaining enough long-term immune pressure to keep the pathogenic loop broken while the immune system resets. The key takeaway is that a modest percentage increase in these high-quality memory cells could translate into millions of additional long-lasting CAR-T cells capable of sustaining control for much longer. Note: This is …...

Votes:

6

0

57

Yahoo Finance

05/13

(Community Post)

some delusion here about the language that the company has used about allo 329...IT IS NOT NEW ...

57

TipRanks News

05/13

Allogene Therapeutics options imply 10.6% move in share price post-earnings

Advertisement Advertisement Allogene Therapeutics options imply 10.6% move in share price post-earnings TheFly A+ A- Pre-earnings options volume in Allogene Therapeutics ( ALLO ) is normal with calls...

57

Yahoo Finance

05/13

(Community Post)

Allogene is trying to move the CAR-T product away from a heavy “sprint killer” configuration and toward more of a “marathon runner” configuration. More Tscm and Tcm cells means more renewable, longer lasting CAR-T biology. Less Temra means less reliance on short-lived terminal effector cells that may hit hard early but burn out faster. For autoimmune disease, that matters because the goal is not just a big early punch. The goal is controlled killing, persistence, re-expansion, and enough long-term pressure to take down the pathogenic immune loops so they are dismantled and lead to a potential immune reset. ALLO-329 is designed to target both major contributors in the pathogenic loop. If the B-cell side and the pathogenic Tfh/Tph helper network are disrupted early, those systems do not simply rebuild overnight. Re-establishing those pathogenic helper networks can take many months, and during that window the immune system may have already shifted …...

Votes:

1

0

57

GlobeNewswire

05/13

Allogene Therapeutics Reports First Quarter 2026 Financial Results and Business Update

This is a paid press release. Contact the press release distributor directly with any inquiries. Allogene Therapeutics Reports First Quarter 2026 Financial Results and Business Update Allogene Therape...

57

Yahoo Finance

05/13

(Community Post)

- **Net loss**: **$42.6 million** ($0.18 per share) — in line with consensus expectations (\~$0.18–$0.19 loss). - **R&D expenses**: $32.0 million (includes $2.7M non-cash stock-based comp). - **G&A expenses**: $14.1 million (includes $5.6M non-cash stock-based comp). - **Cash position**: **$266.9 million** as of March 31. - **Post-earnings boost**: April 2026 public offering added **$200.4 million** gross proceeds → **cash runway extended into Q1 2029**. - **2026 guidance**: Modestly raised operating cash expenses to \~$150–165M (GAAP op. ex. \~$210–225M, incl. \~$35M non-cash SBC)....

57

Yahoo Finance

05/13

(Community Post)

so, patients are resolving quickly, we should see poc in 3 months with complete immune reset...said by the following...

57

TipRanks News

05/13

Allogene Therapeutics increases 2026 operating cash expense guidance

Advertisement Advertisement Allogene Therapeutics increases 2026 operating cash expense guidance TheFly A+ A- Based upon the company’s current forecast for the overall timing of the ALPHA3 program, it...

57

Yahoo Finance

05/13

(Community Post)

## Did you hear that hanasi? They believe their probability has gone up for Early BLA submission for Alpha3. I have already done the numbers on this board, and they come in for passing the statistical boundary at Interim Analysis in mid 2027. I am not the only one believing this, the executives believe it at Allogene, and it seems like the analysts are aware of this as well. Keep in mind they have just told us that enrollment is robust for Alpha3 now. We can see a shift earlier in timeline in the interim if enrollment goes up by 2 patients a month. Even Geoffrey said they would submit the BLA ASAP after interim or primary analysis....

Votes:

8

0

57

Yahoo Finance

05/13

(Community Post)

[@50844](mention://user/8a1eb7bf-796f-4f78-9ef4-5773cf9495ae) This was a very important comment, and seeing it in both the LD (a combined 6 at 20M and 40M) and NO-LD (3 at 20M) cohorts is very positive. The magic number for ALLO-316 was 80 million cells. They are dosing that now. They are very happy with ALLO-329 both with patient enrollment and trial site activation. Zach stated they have high Tier 1 sites ready to be added and will finish their targeted trial site activations soon. The 1 million cells per Kg body weight might hold true here for ALLO-329. That would usually range between 60 million to 80 million cells for adults....

Votes:

6

0

57

Yahoo Finance

05/13

(Community Post)

As I posted last week, no transaction before 2027/2028. Capital was raised because the opportunity presented itself after the outstanding MRD data. Could not wait for ALLO-329 data; they may or may not be presented in July 2026. They can not get below 12-16 months of available cash. There has been tremendous progress, but it will be challenging to keep stock at this range through the 4th quarter. Expect a lot of bumpiness that can present opportunities. On another note, our resident expert again deleted most of its posts, but here is a selection of posts and targets before deletion: May 10, 2026 “…there is an early deal for Allogene in 2026, I believe the first realistic window would be the week of June 22nd to June 26th following the ALLO-329 PoC readout…” May 2 “…I have Alpha3 already in the CHECKED box column for Strategic Interest…” April 10 “… …...

Votes:

1

0

57

Yahoo Finance

05/13

(Community Post)

One thing that really stood out to me other autoimmune CAR-T programs are using much higher doses, some even over 1 billion cells, while ALLO-329 is still only at 20M 40M cells and they’re already talking about “signs of clinical activity.” If they’re truly seeing biological effect at these low dose levels, that could end up being a pretty big deal....

Votes:

2

0

57

Yahoo Finance

05/13

(Community Post)

I thought it was interesting when David Chang was asked about partnerships and basically said it doesn’t make sense right now and that they want to continue advancing the programs. Is that a good thing or a bad thing? Curious how others interpret that....

Votes:

1

0

57

Yahoo Finance

05/13

(Community Post)

## hanasi, no more denying Early BLA. Enrollment is robust for Alpha3. Organizations that have multiple community centers are adding more of their sites to the trial. More sites are adding since the FA because of the results and clean safety profile. South Korea and Australia are adding sites. More sites are being added. That means Cema-cel could commercialize in 2027! ## hanasi, no more denying Early BLA....

Votes:

2

0

57

Yahoo Finance

05/13

(Community Post)

Again, I caution members of the board: the price tomorrow is irrelevant; the market needs time to digest and reach the right balance. On the one hand, a lot of brilliant progress in both programs and a strong balance sheet to carry us to first quarter 2029 vs a delay of schedule by two quarters (this is the second schedule delay, the first being in Cemacel in 2025.) it will take a while to flush through this - the price of importance is towards the end of next week Thursday and Friday. For me, the first impression is to put more emphasis on the progress than the delay. Good luck....

57

Yahoo Finance

05/13

(Community Post)

Two things caught my attention. One, with the increased interest and enrollment in alpha 3 they may see a statistically significant hazard ratio less than 0.5 by interim analysis. Fingers crossed Two, everyone’s favorite analyst Brian Cheng of MS asked why the delay in announcing the AI updates from June to Q4, David Chang said in alpha 316 and with Cemacel, 80 million to 120 million cells were the range where they saw “activity”. Basically, at 20 and 40 million cells, although safe and shows positive activity, it looks like Chang is expecting results he wants from 329 to show up at higher cell count. More waiting for now....

Votes:

3

0

57

Yahoo Finance

05/13

(Community Post)

Lastly, this is how I see the pricing from now through the 4th Quarter ALLO-329 update and preliminary Cemacel EFS readout: Below \~$2 → market pricing high failure risk $2–3 → “wait and see.” $4–6 → pricing in real probability of success $10+ → requires clear clinical validation And to our resident expert, give it a break - you can not post BLA submission and FDA approval in 2025 and 2026 and call anyone who suggested BLA submission at the earliest 2027/2028 as shorts; to now suggesting you've always been calling early BLA submission in 2027? Get help!...

Votes:

2

0

57

Yahoo Finance

05/13

(Community Post)

## hanasi, explain the delay? Is this really a delay or early notification of how a first in human phase 1 trial is suppose occur? There are nine patients dosed for the Resolution trial. That in itself is a great accomplishment across three indications. There are 13 trial sites. Operationally this is moving along at a very fast pace. Investigators are excited about the trial with early clinical activity and safety at the DL1 and DL2 dosing levels. This is normal progression of a phase 1 trial with the first dose levels that are very low because safety is first and foremost. Why wait and tell us this in a month that there is early clinical activity. It is a positive thing there is clinical activity in both arms. That means at 20 million cells the No-LD arm has early clinical activity. If there was no activity, that would be …...

Votes:

2

0

57

Yahoo Finance

05/13

(Community Post)

## hanasi, I did not suggest Early BLA. It was brought up by Geoffrey Parker on the call tonight. It was brought up by an analyst tonight to the executives. Lastly, David Chang said their probability of passing the statistical boundary at the Interim EFS mid 2027 has gone up. Who were these three people talking to? Ghosts on the other line or to investors? hanasi, Early BLA was discussed tonight and I did not bring it up on the call....

Votes:

2

0

57

Yahoo Finance

05/13

(Community Post)

[@hanasi_u_4i2q9n](mention://user/4eacaade-50a2-4304-a9a8-9a4998446062) yeah, I’m gonna step away from this message board until Q4 2026 to get the real PoC update on 329 (it didn’t show up today and June announcement has been cancelled); and it doesn’t look like cema-cel will be given RMAT until the FDA sees data from the interim EFS analysis mid 2027. Good luck to us all....

Votes:

1

0

57

Yahoo Finance

05/13

(Community Post)

[@rocco72376](mention://user/991c1f9c-e3be-4e4a-bb3d-adbe4b929f4c) yup; they were uber conservative with safety. So the real 329 PoC announcement won’t happen until Q4 2026, when they’re dosing the 80 to 160 millions cells doses. Until then, good luck....

57

Yahoo Finance

05/13

(Community Post)

Someone should share with our resident expert that the ALLO management has directed since 2025 interim EFS in midyear 2027 and final EFS in 2028; and now suggesting results will be strong enough in 2027 to submit an early BLA is not in the same universe as our resident expert who was promoting an early BLA submission in 2025 and 2026. Get help!...

57

TipRanks News

05/13

Analysts’ Top Healthcare Picks: Allogene Therapeutics (ALLO), Evommune, Inc. (EVMN)

Advertisement Advertisement Analysts’ Top Healthcare Picks: Allogene Therapeutics (ALLO), Evommune, Inc. (EVMN) Brian Anderson A+ A- There’s a lot to be optimistic about in the Healthcare sector as 3...

57

Yahoo Finance

05/13

(Community Post)

[@hanasi_u_4i2q9n](mention://user/4eacaade-50a2-4304-a9a8-9a4998446062) Rennie Benjamin asked the key question on the call: after seeing the Alpha3 MRD differential, has the probability of success at the interim analysis increased versus what Allogene originally modeled when designing the study? David Chang’s answer was highly significant. He stated the study was originally powered around a hazard ratio of 0.5, but based on the MRD clearance differential they are now extrapolating toward a potentially much lower hazard ratio. He further stated that if this trend continues as enrollment progresses, the probability that the interim analysis reaches statistical significance becomes “very significant.” That is not management simply saying they liked the MRD data. That is management explicitly signaling that the observed biology may be translating into a materially stronger EFS expectation than the original pivotal assumptions. In practical terms, stronger MRD-driven event separation can increase the probability of crossing the interim statistical boundary and strengthens the possibility …...

57

Yahoo Finance

05/13

(Community Post)

[@hanasi_u_4i2q9n](mention://user/4eacaade-50a2-4304-a9a8-9a4998446062) Don't be fooled by the hanasi - Cid interactions - pure Short Interest. This Cid character does not know what he is talking about with regards to early approval at Interim EFS. He is putting up a road block that does not exist, it is the same stuff these Short Interest characters have been doing on this board for a long time now. Total junk information from Cid....

57

Yahoo Finance

05/13

(Community Post)

Our resident expert is posting from multiple of its 25 profiles. The story won't change; your 2025 & 2026 BLA submissions and FDA approval do not align with Management's consistent timeline. The ALLO-329 POC delay from June 2026 to the fourth quarter 2026 will have a stock impact and increase risk. Maintaining our $2-$3 price range till July 2027 - Cemacel's preliminary EFS analysis - will be challenging and extremely volatile. If Citadel and Frazier reduce their position in the third quarter of 2026, expect new lows. Good luck!...

Votes:

1

0

57

Yahoo Finance

05/13

(Community Post)

Overall tremendous progress and the extension of the data readout justifies the capital raise as time is $. I have seen this playbook many times and are extremely bullish I think the stock will bounce around this area and in December it could be parabolic. We are sailing a big ship and need the water to be deep...

Votes:

1

0

57

Yahoo Finance

05/13

(Community Post)

[@hanasi_u_4i2q9n](mention://user/4eacaade-50a2-4304-a9a8-9a4998446062) This is what the Short Interest does. They scare people with propaganda even when the data is strong and enrollment is robust. This guy will still be towing the same line with early approved next year. Its in the transcript along with Management talking about it. They are funded until Q1 2029 (2.5 yrs from now) and if they commercialize next year then what happens to this guy's story? Don't listen to the Short Interest - they are here to scare you like this guy....

57

Yahoo Finance

05/13

(Community Post)

You can use as many profiles as you like, but everyone knows who you are and realizes you have zero credibility. The fact remains that many here did not understand why raise at $2.00/share, leveraging MRD, only when POC for ALLO-329 is right around the corner in July? And today's update responded clearly that the earliest POC for ALLO-329 will take place in the 4th quarter of 2026, and thus the Company had no choice but to raise st $2.00/share in April 2026. Our resident expert deleted most of its messages. Still, many here anticipated that, in addition to the POC for ALLO-329 to be announced in July 2026, our resident expert predicted ALLO would expedite Cemacel and file the BLA in 2026, and also suggested that an acquisition of ALLO is most likely in June 2026. Very similar to its posts in 2025, all intended to mislead and stray …...

Votes:

1

0

57

Yahoo Finance

05/13

(Community Post)

## hanasi, get it in your head. ## Early BLA in 2027 is coming. Robust enrollment is happening. More Alpha3 trial sites are coming online. Finally, the true design of Alpha3 is coming into play as I originally talked about. The results have spoken for themselves and investigators want in. The low tumor burden MRD setting was a great design and the numbers will bear it out for an Early BLA in 2027. I have always stated an Early BLA would come out of Alpha3, and it will be proven correct in mid 2027 or earlier with robust enrollment. Alpha3 has been significantly de-risked. I know that pains you hanasi, but I will keep repeating it for you and all your Short Interest buddies to take it in. We already know Rennie Benjamin and David Change talked about early approval during the call for 2027. Then is was Geoffrey Parker's …...

Votes:

3

0

57

Yahoo Finance

05/13

(Community Post)

Fascinating resident expert is at it again with its 20-some profiles. Here is the transcript explaining the timeline per Management: “…Hi, this is Jeff on the Cash Runway. As we discussed in the script, our current Cash Runway, based on the addition of the capital added in the recent financing, the $200 million financing, takes us into the first quarter of 2029. And during that time, we intend to complete the Alpha 3 study. So as you know, we anticipate finishing enrollment at the end of 2027. We anticipate an interim analysis on EFS in mid-27, a primary analysis in mid-28, and the filing of the BLA as quickly as possible based on the results of those analyses. So it really is focused on covering Alpha 3 as well as completing this Phase 1 resolution study for 329…..” Good luck!...

57

Yahoo Finance

05/14

(Community Post)

Dr. Chang said - “the investigators are calling us and telling us that they're seeing that they would not have expected to see in any setting, I mean, that I would view as a highly encouraging early signs.” \- They explicitly admitted the starting dose was probably too low \- So the company is now entering what they themselves view as therapeutically meaningful exposure territory at 80 million cells \- The company repeatedly emphasized clinical activity in BOTH arms \- The safety profile sounds better than many expected \- The Q4 shift now makes more sense After reading the full transcript carefully, I no longer think Q4 should be interpreted negatively. The logic appears to be: Current state - Strong early qualitative activity - Very low starting doses - Tiny patient numbers - Ongoing escalation - Good safety - No-LD activity already visible Therefore Management wants: - higher-dose cohorts, - …...

57

GuruFocus.com

05/14

Allogene Therapeutics Inc (ALLO) Q1 2026 Earnings Call Highlights: Promising Trial Results and ...

Allogene Therapeutics Inc (ALLO) Q1 2026 Earnings Call Highlights: Promising Trial Results and ... GuruFocus News Thu, May 14, 2026 at 8:00 AM GMT+3 4 min read ALLO This article first appeared on Guru...

57

Yahoo Finance

05/14

(Community Post)

## hanasi you lie. You do that all the time, like telling us all patients in Alpha3 must undergo 12 months of observation before interim EFS. You do not understand the trial setup of you just make up lies to fit your extension of time lines. Geoffrey Parker said the following precisely in the way that it could happen. He said the following. "We anticipate an interim analysis on EFS in mid 27, primary analysis in mid 28 with the filing of the BLA as quickly as possible based on the results of those interim or final analysis." **- on the results of those interim OR final analysis -** **He did not use an AND, he used an OR.** **Get it right and do not try to fit it in to your narrative.** **EARLY BLA 2027**...

57

Yahoo Finance

05/14

(Community Post)

After listening to the full conference call and reading the transcript carefully, what is coming out of ALLO-329 is positive. Dr. Chang made a very important statement on the call telling us investigators are seeing things they would never have expected to see in any setting. He said this was very encouraging to hear. It is definitely surprising language for a first-in-human autoimmune CAR-T study operating at very low starting doses. The company also explicitly admitted that the initial 20 million cell dose was likely lower than necessary therapeutically. Despite that, they are already seeing clinical activity in both arms including No-LD at 20 million cells with a favorable safety profile. That matters. Allogene is now escalating into the dose range where they historically observed stronger activity in prior programs like ALLO-316. DL3 is already dosing at 80 million cells, which also aligns much more closely with historical autologous autoimmune …...

57

Yahoo Finance

05/14

(Community Post)

**Investigators are seeing things they would never have expected to see in any setting.** When I first saw what this dual CAR-T could do to the pathogenic loops in theory, I thought we might see some things never seen before in autologous CAR-T for autoimmune disease. I even mentioned it on this board. Hopefully, we see much more of it....

57

Yahoo Finance

05/14

(Community Post)

The call materially strengthened the investment thesis across three dimensions. The ALPHA3 probability of success has increased in management's own estimation. ALLO-329 is progressing faster than expected with early clinical signals at doses management believes are probably below therapeutic threshold.....meaning in essence that better results are likely as they escalate to 80-120 million cells. The cash position removes all near-term risk. That's my take on the headlines....

Votes:

3

0

44

Ticker Report

05/14

Allogene Therapeutics (NASDAQ:ALLO) Announces Earnings Results, Beats Expectations By $0.01 EPS

Allogene Therapeutics (NASDAQ:ALLO – Get Free Report) announced its earnings results on Wednesday. The company reported ($0.18) earnings per share (EPS) for the quarter, topping the consensus estimate...

57

TipRanks News

05/14

Piper Sandler Sticks to Their Buy Rating for Allogene Therapeutics (ALLO)

Advertisement Advertisement Piper Sandler Sticks to Their Buy Rating for Allogene Therapeutics (ALLO) TipRanks Auto-Generated Intelligence Newsdesk A+ A- In a report released today, Biren Amin from Pi...

57

TipRanks News

05/14

Analysts Offer Insights on Healthcare Companies: Allogene Therapeutics (ALLO), Biogen (BIIB) and COMPASS Pathways (CMPS)

Advertisement Advertisement Analysts Offer Insights on Healthcare Companies: Allogene Therapeutics (ALLO), Biogen (BIIB) and COMPASS Pathways (CMPS) Brian Anderson A+ A- There’s a lot to be optimistic...

57

Yahoo Finance

05/14

(Community Post)

Excellent update yesterday. I’ve listened to it twice and the biggest thing I came away with: The company sounds like it believes it has crossed the threshold from “does the construct work at all?” to “how strong and durable is the effect?” It’s no longer about the PoC (that appears to be a done deal) but about maturing the data enough to provide a comprehensive dataset in Q4. Upwards and onwards 🍻🍻...

Votes:

5

0

57

Yahoo Finance

05/14

(Community Post)

[@stockgenious](mention://user/8fbb03c8-6ddd-43ce-b51e-5f5656845013)--I think the market will react to the fact that this is dead money for another 6 months and we are in danger of missing the patent cliff year completely if they continue to move the goal posts which seems to be the M.O. here. Why buy now when you can wait and probably catch it under $2. I still believe in the science, but I clearly bought in way too soon (2023). It just hurts......

Votes:

3

0

48

24/7 Wall St.

05/14

Big Pharma’s 5 Hottest Biotech Hunting Grounds: Meet the Category Leaders

Big Pharma’s 5 Hottest Biotech Hunting Grounds: Meet the Category Leaders Trey Thoelcke Thu, May 14, 2026 at 8:20 AM CDT 5 min read LEGN VKTX LNTH ALLO ADCT Quick Read Biotech dealmaking has accelerat...

57

Yahoo Finance

05/14

(Community Post)

[@tae3694](mention://user/d8f9140d-2061-405f-97bd-3ddb48348388) reaction is to the POC date moving to Q4 and assuming that because of this, no short term jump in share price will take place and the “day trading” money is moving elsewhere. A short sighted move, because once we hit Q4…this will fly....

Votes:

4

0

57

TipRanks News

05/14

Analysts’ Opinions Are Mixed on These Healthcare Stocks: Pharvaris (PHVS) and Allogene Therapeutics (ALLO)

Advertisement Advertisement Analysts’ Opinions Are Mixed on These Healthcare Stocks: Pharvaris (PHVS) and Allogene Therapeutics (ALLO) Catie Powers A+ A- Companies in the Healthcare sector have recei...

57

Yahoo Finance

05/14

(Community Post)

The science is completely dead. None of the data supports durable efficacy, persistence, or meaningful clinical benefit. The platform appears unable to generate sustained long-term control, and the proposed mechanisms are not translating into real therapeutic outcomes. At this stage, the entire approach looks fundamentally broken rather than delayed. ...

57

Yahoo Finance

05/14

(Community Post)

They say **imitation is the sincerest form of flattery.** **Obviously the character below trying to post as me is very funny and takes after Mo.** **ALLO-329 - Investigators are seeing things they would never have expected to see in any setting. This has me excited!**...

Votes:

1

0

57

Yahoo Finance

05/14

(Community Post)

They gave everyone a peak into the ongoing ALLO-329 trial…The bear thesis that the Dagger technology would fail to prevent host rejection has taken a massive hit. The "Zero Lymphodepletion" dream survives. They confirmed that 3 patients were successfully dosed with 20 million cells and absolutely no fludarabine or cyclophosphamide pre-conditioning. They are seeing "favorable tolerability" and "early signs of clinical activity."...

57

Yahoo Finance

05/14

(Community Post)

Keyser is acting more like a promoter than an objective analyst at this point. I used to trust the DD, but the constant spin, selective interpretation of data, and dismissal of obvious problems makes it feel like he’s pumping the stock instead of giving people an honest assessment. The science keeps weakening, timelines keep slipping, and every setback gets reframed as bullish. That’s not transparency that’s narrative management. People are risking real money based on this....

57

Yahoo Finance

05/14

(Community Post)

This is what they're currently working on...dosing patients at the 80M "Reduced LD" dose, wait to clear their critical 28-day safety window without severe adverse events, the trial protocol will unlock the 80M "Zero LD" arm (what Roberts refers to as being "close behind"). This explains the delay of readout...David mentioned he wanted to release meaningful data....

57

Yahoo Finance

05/14

(Community Post)

## What just happened in yesterday's quarterly call: (1) Cash runway into Q1 2029 (the most important "new" announcement); (2) Which effectively means the company has enough money to see cema-cel through the interim EFS analysis mid 2027 without any financial pressure (of being under 12 months cash runway); the investment thesis remains, that cemal-cel alone (with current fully diluted outstanding shares) put a baseline value of $30 per share when cema-cel is approved; (3) ALLO-329 is well tolerated at the 20 and 40 million cell doses, but obviously these low doses did not show sufficient B cell depletion (and correspondingly sufficient CAR T expansion) to be worth talking about in June; so the June announcement has been replaced with a Q4 2026 announcement; this is what I had feared, that the starting doses are too low; but management is still very optimistic; they indicated that early clinical efficacy signals …...

Votes:

3

0

57

Yahoo Finance

05/14

(Community Post)

The thing that is VERY obvious here is this: if Allo 329 had achieved results clearly superior to programs like FT819, they would have released the data already, PERIOD. What likely happened is that after dosing the initial patients, they saw a response , but one that was far more underwhelming than expected. Otherwise, why continue escalating doses instead of confidently leaning into the early data? The expansion of trial sites after initial dosing says a lot. Enrollment in autoimmune disease trials is extremely difficult, and opening more sites strongly suggests they needed broader recruitment to continue the escalation strategy. Even getting one patient per site can be considered a win in this space. The dose-escalation design itself also tells you a lot about the safety concerns around targeting T cells. This is not a trivial therapy from a safety standpoint....

57

Yahoo Finance

05/14

(Community Post)

That is exactly why they started at only \~5% of the cell dose typically used in allogeneic therapies and are moving upward cautiously. If the therapy were producing exceptional efficacy with a clean safety profile, the tone and pace would likely look very different. And ultimately, if they cannot achieve something close to a complete immune reset, they have no real place in this competition. Management understands this very well, which is likely part of the reason for the cohort delays. To move from 20M → 40M → 80M → 120M cells across three autoimmune indications, both with and without cyclophosphamide, they likely need at least \~24 patients. That means each site would need to contribute multiple patients — not easy in AID recruitment. And once they reach higher dose levels, if the safety profile begins to look materially worse than the benchmark being set in autoimmune therapies, they will …...

57

Yahoo Finance

05/14

(Community Post)

I agree with many of the points and posts on ALLO-329, but it will be challenging to incorporate them as is into ALLO's valuation thesis. I do think Cemacel is real, and if the preliminary EFS analysis supports/strengthens the data demonstrated at preliminary MRD clearance, the $18 buyout in 4th qtr 2027 is in play. Yes, it's most likely dead volatile money until then, but 8x for Cemacel is real / timing when to get in to capture it could be challenging. We can't go back in time, but May 2026 to Dec 2027 - 8x in the speculative bucket is ok with me. Obviously, if I were in the red on the investment, I would exit here and consider getting back in August with a loss asset carryforward and new investment forming a new basis. Until further data is provided, my value allocation to Allo-329 is $0. My investment …...

57

Yahoo Finance

05/14

(Community Post)

[@hanasi_u_4i2q9n](mention://user/4eacaade-50a2-4304-a9a8-9a4998446062)would you for once stop talking you robot? Always about the same and wishing good luck at the end. Keyser stopped pumping and you here every day to remind about schedules and price targets, get a life buddy....

57

TipRanks News

05/14

Allogene’s UNIVERSAL Trial Completion: What ALLO-715 Data Could Mean for Investors

Advertisement Advertisement Allogene’s UNIVERSAL Trial Completion: What ALLO-715 Data Could Mean for Investors TipRanks Clinical-Trials-Auto-Generated Newsdesk A+ A- Allogene Therapeutics (ALLO) annou...

57

Yahoo Finance

05/14

(Community Post)

I have been a buyer of ALLO from its high flying days in 2021 when it was trading at $38 a share. Trust me when I say I have learned to be patient with this stock. But, importantly, if you care at all about day-to-day, week-to-week, or even month-to-month movements of this stock you are investing in ALLO incorrectly. The data will drive the price of the stock, and that takes time. Think about it this way - if the interim analysis in 2027 is positive, does it matter what price the stock price is at that time? It could be 50 cents, or 8 dollars, and it will still explode upwards as the adjusted valuation is priced in. hanasi (who is definitely a character who probably needs a hobby other than weirdly posting on this board 8 times a day in a consistently slightly negative light) is implying that …...

Votes:

2

0

57

Yahoo Finance

05/14

(Community Post)

[@jerry1224](mention://user/6302d6bb-9bf4-40e9-8d35-7bc837700ecb) I don't disagree with your thesis. It aligns well with what I attempted to communicate. My investment is intact, nothing has changed my sentiment, and I look forward to the preliminary Cemacel Alpha-3 EFS analysis midyear 2027. I couldn't care less how the stock performs between Management's data updates, if the 4th quarter ALLO-329 update is positive, even better. My investment is long-term, all tranches beyond 12 months, it's a full position, and yes, it's dead money for me - I am not trading or hedging around it. I don't recommend anyone try to time when this investment might hit. Btw, I feel comfortable practicing my English writing here daily. After reading the other posts, it's obvious that not very educated or experienced individuals are here, so I'm very comfortable. Good luck!...

57

Yahoo Finance

05/14

(Community Post)

Finally getting some traction, going straight to the woodshed where it belongs. I am hoping this craters more during the day, so our Split‑Tongue Long‑Horizon Continuous‑Posting Engagement Strategist can post more about his long term investment he does not care about anymore 🤣🤣🤣...

57

Yahoo Finance

05/14

(Community Post)

## Early BLA 2027? As discussed in the Q1 conference call between analysts and executives. Also, Geoffrey Parker made it very clear that they will submit a BLA immediately after the Interim or Primary EFS. The foundation and starting point of \~42% MRD Delta already points to a potential early BLA submission in 2027. David Chang said it in the Q1 conference call that their probability of achieving this has gone up. ...

57

Yahoo Finance

05/14

(Community Post)

Unfortunately, we will not know whether Frazier has reduced its position until August… they added the shares in April and are below 5% - no reporting required other than quarter end. Monitor the volume on the down days and the up days; the differential matters. Good luck!...

57

Yahoo Finance

05/14

(Community Post)

Justina, what do you currently have in your portfolio? I liquidated almost everything this week, so I’m sitting on a lot of cash and watching for opportunities. I have a feeling the next two quarters could make a lot of stocks very cheap. Some of my previous plays: - MRAM (Everspin) : - STX : - KYTX : - FATE: - Allo …and a few others that I exited earlier. What’s currently on your watchlist?...

57

Yahoo Finance

05/14

(Community Post)

Another thing everyone should seriously consider here: Allogene now has plenty of cash, expanded sites aggressively, and recently posted 25+ senior roles…yet almost none of them are related to autoimmune disease. If they were truly seeing exceptional results with ALLO-329 and were fully confident this was part of the future of the company, you’d expect a hiring wave around AID development, operations, clinical leadership, commercialization…something. Instead? Crickets. Who exactly is supposed to run these massive autoimmune trials long term , the cleaning staff? And here’s the other uncomfortable point nobody wants to say out loud: if the MRD data had truly “validated” or materially de-risked the pipeline, big pharma would have piled into the last offering aggressively. 🤡🤡🤡🤡🤡🤡🤡🤡...

57

Yahoo Finance

05/14

(Community Post)

Think about it logically. If this company is supposedly heading to $200/share within a year according to some clowns here, buying 40% of the company at around $2 would be the steal of the century. Yet somehow, the market treated it like a distressed biotech financing instead of a generational opportunity and no BP has stepped in.... They still question the durability 🤡🤡🤡🤡🤡🤡🤡🤡...

57

Yahoo Finance

05/14

(Community Post)

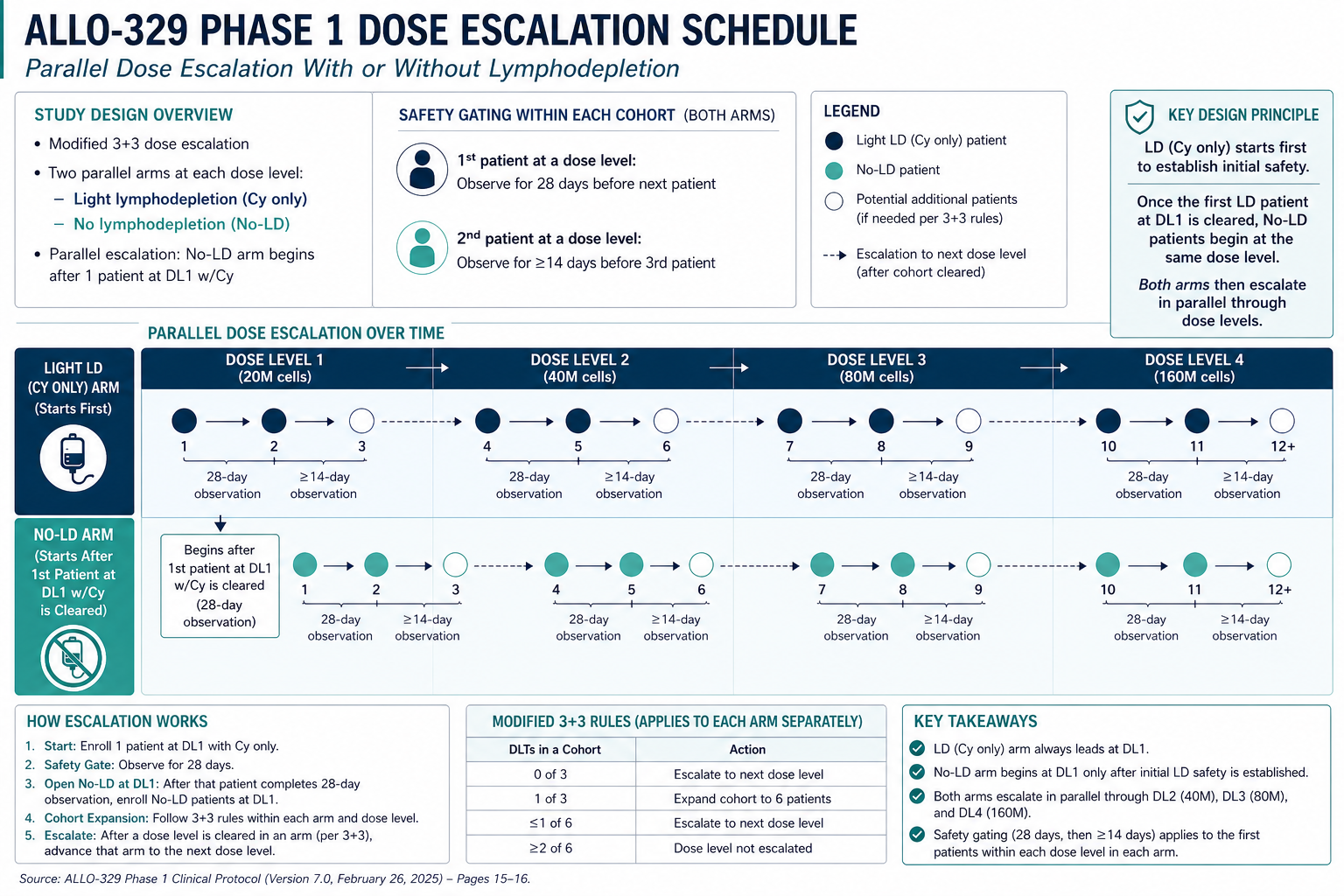

## A dose level comparison. ...

57

Yahoo Finance

05/14

(Community Post)

## Has anybody read the 8-K? It appears Allogene may be restructuring its Asia-Pacific strategy and positioning to retain more direct control over these markets rather than relying on older regional licensing structures put in place years ago under a very different CAR-T environment....

Votes:

1

0

57

Yahoo Finance

05/14

(Community Post)

My crystal ball says, selling intensifies tomorrow and we have first weekly close below signal line since 4Q'25 which would then put a test towards $2 dollars threshold. I am looking forward to see how the price reacts to that price range and if any institutions would be there to scoop up. In the mewntime good luck hanasi, nice haircut you got today - pumping did no good....

57

Yahoo Finance

05/14

(Community Post)

[@justinas47364](mention://user/abb95504-5023-4a17-8ad6-6572099e1e01) They raised capital two weeks ago at $2 share, not because it was valued at $75 a share as you and our resident expert were posting leading up to the mrd reading. Anyone who thought the valuation is greater than $2.00 share post mrd is certainly hurting and should recalibrate their financial acumen. I think until we get additional data prices between $2 to $3 are reasonable and significantly below $2 is a potential buying opportunity for anyone wanting to add to their investment position. Had you read other posts explaining to you why your valuation is way off you would not be in so much pain. No shame in learning all beginners lack experience and yes you will learn from your losses and waste your wins. Good luck!...

57

Yahoo Finance

05/14

(Community Post)

## Hiring is for all programs. Mo keeps trying to frame the recent hiring activity at Allogene as only supporting Alpha3/Cema-cel. I do not think that interpretation matches either the recent conference call, the open positions being added on LinkedIn, or the broader direction outlined in the 10-Q. What I see instead is a company increasingly organizing around 3 major strategic pillars simultaneously: 1. Cema-cel / Alpha3 as the registrational oncology anchor with growing global infrastructure and expanding MRD-driven development. 2. ALLO-329 as the lead autoimmune platform where investigators are already reporting unexpected clinical activity at very low doses including No-LD, while the company escalates into the more historically meaningful 80M+ exposure range. 3. BCMA/CD70 as a next generation platform expansion that potentially broadens opportunity into Multiple Myeloma and beyond. The 10-Q also showed continued global operational expansion, restructuring of older regional licensing agreements, and ongoing investment into platform scalability. …...

57

Yahoo Finance

05/14

(Community Post)

[@cuda7125](mention://user/069f5451-ce06-40cb-b4df-ff6da97e14e9) Wish I could agree wichu Cuda, but I'm not entirely sure about the POC part, and that was why there was a HEAVY emphasis in the Q and A about 329. The answers were STRONGLY optimistic about the operational side, the enrollment, # of sites, etc. The wording was a bit more guarded re the science...."encouraging" or "very positive" from the researchers/clinicians, but to me, you have to balance out the guidance the company gave that changed more for POC to "safety" and "escalating dose". At 9 patients, they CLEARLY did not feel they could release the reset data and that is the bar that must be cleared. I do not feel we will definitively know the POC part until December..... I think that data will CLEARLY be a binary event in how the market perceives fair share price.........

57

Yahoo Finance

05/14

(Community Post)

## Allogene was never guiding for EULAR. That does not line up at all; they needed the shareholders meeting to take place first. The best timing would have been to release data during the week of June 22-25. matt I think you are incorrect....

57

Yahoo Finance

05/14

(Community Post)

Q1 2025: Under the explicit “ALLO-329: CD19/CD70 Dual CAR with Dagger® Technology in AID” header — “The Company has shifted timing for its first update to this program to 1H 2026 to allow for both biomarker and clinical proof-of-concept data.” Q2 2025 (Aug 2025): Under the ALLO-329 section — “The first clinical update, expected in 1H 2026, will include biomarker data and clinical proof-of-concept data.” Jan 2026 catalyst stack press release: “Initial Proof-of-Concept for ALLO-329, the Dual CD19/CD70 AlloCAR T Leveraging the Dagger® Technology to Reduce or Eliminate Lymphodepletion in the Treatment of Autoimmune Diseases, Slated by the End of 1H 2026” Communications PR explicitly states under the ALLO-329 / RESOLUTION header: “Phase 1 RESOLUTION Dose Escalation Rheumatology Basket Trial Actively Enrolling; Initial Data from First Dose Level Expected June 2026 with an Additional Clinical Update Planned for Year-End”...

57

Yahoo Finance

05/14

(Community Post)

I refuse to be a habitual poster on this board, but I will say this - ALLO does not care about the current stock price, and they for sure do not care about you or me. None of the employees have the ticker on their computers, monitoring its every movement and constantly thinking about ways to increase shareholder value or whether a certain decision will raise or lower the stock price. ALLO is filled with scientists who only care about validating the science. They raised cash because ALPHA3 looked good; they are hiring more because ALPHA3 looked good; they consistently tell us that ALPHA3 looks good; and 329 looks good as well and the data in Q4 would be more robust than anything provided in June (so calm down about the June readout, any gains you would have had are just temporarily delayed at worst, and compounded at best). The …...

Votes:

2

0

57

Yahoo Finance

05/14

(Community Post)

My take on the stock: we’ll revisit $1.50 and likely stay there for about 8 months. Then they’ll submit their BLA to the FDA in 2029 and, as I’ve always said, potentially gain approval by 2031. Until then, I think we stay under $2. This is my expert opinion. Buckle up, and good luck....

57

Yahoo Finance

05/14

(Community Post)

[@keyser96770](mention://user/282a52a8-ff41-4466-8355-3413686b40f4) Give it a rest, man. Nobody believes you and your hundred fake profiles. You’re bullish and bearish at the same time nobody is listening to your fake analysis and fake data. I assume you’ve lost all credibility with most of the experienced investors on this platform....

Votes:

1

0

57

Yahoo Finance

05/14

(Community Post)

## Would you expect the 20M dose? ## In any setting? The more I study the ALLO-329 protocol structure and management commentary, the more I think the first 9 patients followed a very conservative, stepwise de-risking approach. It appears Allogene first established a Light-LD safety/biology anchor at 20M, then tested 20M No-LD, followed by escalation of the Light-LD arm to 40M. Importantly, the protocol allows that sequence. No-LD only required the first 20M Light-LD patient to clear the initial 28-day safety window - it did not require immediate parallel enrollment. That matters because 20M No-LD is probably the hardest possible setting for an allogeneic CAR-T to show meaningful biology. Conventional assumptions would predict limited expansion, rapid host rejection, shallow B-cell depletion, and minimal clinical effect. Instead, investigators reportedly saw things they “would not have expected to see in any setting.” In my view, that language becomes much more meaningful if …...

Votes:

1

0

57

Yahoo Finance

05/14

(Community Post)

[@jerry1224](mention://user/6302d6bb-9bf4-40e9-8d35-7bc837700ecb) I agree with most of what you stated except after listening to the conference call yesterday it appears as though that management also cares about "non cash stock based compensation". I heard some exorbitant numbers thrown around but I haven't done a comparison YOY so I'll wait to REALLY complain until I see it on paper. I've taken some chances on multiple clinical stage companies in the past and "offerings" seem to be followed up with raises and bonuses frequently. You really have to watch that because they can drain what should be R&D capital very quickly when they start doling out executive level compensation for mediocre results. Time will tell but that's just it,,,,,,"time",,,,and they apparently are going to need a while to stir up some REAL interest....

{kind=link}

Il me semble que cette histoire de clonage de voix à partir d’un simple "allo" a déjà été debunkée, à classer comme légende urbaine.